Across the country in Federal Fiscal Year 2021, there were 588,229 victims of child neglect and abuse based on reports from states, the District of Columbia, and the Commonwealth of Puerto Rico. That averages to a victimization rate of 8.1 per 1,000 children.[1] Of the close to 600,000 reports of child maltreatment three-quarters (76%) were cases of neglect compared to 16% that were physical abuse and 10% which were cases of sexual abuse.[2]

Young children continue to be a greatest risk of abuse or neglect. [3]

There are also sharp racial differences in the reported cases of maltreatment. Overall, the victimization rate is highest for American-Indian or Alaska Native children (15.2 per 1,000 children) followed by African-American children (13.1 per 1,000). The victimization rate for Hispanics was 7.7 per 1,000 and for whites 7.1 per 1,000. That said, the victimization rates listed in a 2023 report from the U.S. Department of Health and Human Services regarding Illinois children by race and ethnicity are[4]:

- 27.4 per 1,000 for Black children,

- 10.1 per 1,000 for Hispanic children and

- 10.9 per 1,000 for white children

In many cases of neglect, poverty is a significant factor. In fact, a number of academic studies have documented that the social determinants of health that include poverty, parental educational attainment, housing instability, food insecurity, and uninsurance are associated with child maltreatment.[5] Furthermore, as adults, maltreated children are at increased risk for behavioral, physical and mental health problems that include depression, obesity, high-risk sexual behaviors, and alcohol and drug misuse. [6]

________________________________________________________________________________________________________________

Poverty versus Child Neglect:

Much of the data cited here is based on state reports of child abuse and neglect. Neglect is based on state and federal definitions.

The CDC use the following definition of child maltreatment as:

Any act or series of acts of commission (physical abuse, sexual abuse, psychological abuse) or omission (physical neglect, emotional neglect, medical/dental neglect, educational neglect, inadequate supervision, exposure to violent environments) by a parent or other caregiver that results in harm, potential for harm, or threat of harm to a child.

Child Maltreatment Surveillance, Uniform Definitions for Public Health and Recommended Data Elements, Centers for Disease Control and Prevention, January 2008

However, a pair of former federal officials also note:

“Poverty is a risk factor for neglect, but poverty does not equate to neglect. The presence of poverty alone does not mean a child is unsafe, unloved, or that a parent lacks the capacity to care for his or her child.”

Jerry Milner, Former Associate Commissioner of the Children’s Bureau, U.S. Department of Health and Human Services David Kelly, Special Assistant to the Associate Commissioner

Milner, J. & Kelly, D. (December 2019/January 2020). It’s time to stop confusing poverty with neglect.; Children’s Bureau Express, 2010).

___________________________________________________________________________________________________________________

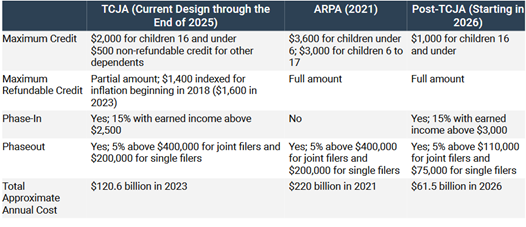

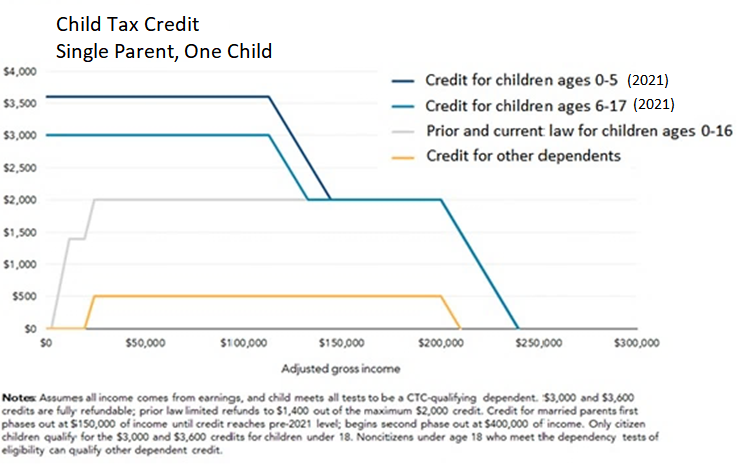

Given the impact of poverty, one cannot ignore the tremendous impact the 2021 enhanced federal child tax credit had in reducing poverty. The enhanced credit not only increased the maximum credit level from $2,000 per child to $3,600 for children under the age of six and $3,000 for children ages 6-17 but it also made the full value of the credit available to more low-income families. It had a dramatic impact on children and families. The U.S. Census Bureau estimates the 2021 expansion of the federal Child Tax Credit lifted 2.1 million children out of poverty.[7] The Census Bureau arrived at this estimate using the Supplemental Poverty Measure.[8]

Unfortunately, Congress authorized this significant anti-poverty measure for only one year (2021) during the height of the pandemic. Since then, with the credit falling back to $2,000, it has not been able to agree on an increase in the credit. The impact of the inaction is significant. Census figures show that, based on the SPM, child poverty increased nationally from 5.2% in 2021 to 12.4% in 2022.[9]

The Census Bureau has not yet released the latest state SPM figures. However, the state supplemental poverty measurement rate from the census bureau went from 12.7% in 2019 for children under age 18 to 5.5% in 2021 (a reduction of 56.7%).[10] It is expected that when the Bureau releases the state 2022 rates later this year, the number will show an increase similar to the national figure.

The Census Bureau numbers out on the official child poverty rates in 2022 show that the child poverty rate for Black Illinois children is four times that of white/non-Latinx Illinois children (9.0% vs 36.1%) and the child poverty rate for Latinx children (18.7%) is more than twice the rate for white/non-Latinx children.[11] Thus, with markedly higher poverty rates, the current rates of maltreatment by race, and poverty being a significant factor in child maltreatment, it would appear Black children are at a higher risk of child maltreatment.

The numbers show the impact additional economic supports such as the Child Tax Credit and the Earned Income Tax Credit can have on reducing poverty and a number of studies point to the correlation between reducing child maltreatment by reducing poverty. The reasons may vary. As a report on economic supports and child well-being from Chapin Hall at the University of Chicago notes, financial supports may reduce parental stress. [12]

Here are just a few of the studies examining the impact of additional economic supports on child maltreatments:

- With the enhanced federal child tax credit, the federal government also advanced half the credit to taxpayers in monthly payments. An examination of data from Georgia hospitals shows the advance payments were associated with fewer child abuse and neglect related emergency department visits.[13]

- Modeling of the Earned Income Tax Credit shows a 10% increase in state EITC benefits was associated with 241 fewer reports of neglect per 100,000 children.[14]

- A refundable EITC was associated with a decrease of 3.1 abusive head trauma admissions per 100,000 population in children aged <2.[15]

- A refundable state EITC was associated with an 11% decrease in foster care entries compared to states without a state-level EITC after controlling for child poverty rates, racial/ethnic composition, education and unemployment. [16]

- An examination of Temporary Assistance for Needy Families data from 2001 to 2010 found that increases in maximum allowable TANF cash benefits and greater access to TANF benefits decreased mothers’ self-reports of physical maltreatment.[17]

In its review of state policy options to increase access to economic supports as a child welfare prevention strategy, Chapin Hall lists a number of recommendations that include:

- Establishing a refundable state level Child Tax Credit,

- Establishing a refundable state-level Earned Income Tax Credit (not only increasing the level of the credit but also implementing measures to increase EITC uptake such as supplied fax filing),

- Increasing the state minimum wage (currently $14 per hour and slated to go $15 next year),

- Implementing paid family leave and

- Better leveraging funding opportunities to support well-paying , stable employment – including redesigned TANF work programs.

Other measures cover child care, housing, medical care, the Supplemental Nutrition and Assistance Program and the Women Infants and Children (WIC) Program.

Illinois currently has a state EITC (worth, in Tax Year 2024, 20% of a taxpayer’s claimed federal EITC) but could take a major step forward with the establishment of a state Child Tax Credit. Fourteen other states now have some form of a state Child Tax Credit.[18] As the research cited here indicates, a child tax credit can not only provide greater economic security to working families but potentially reduce family stressors and in the process reduce the number of child maltreatment cases.

Written by Tim Franklin and Mitch Lifson.

[1] U.S. Department of Health & Human Services, Administration for Children and Families, Administration on Children, Youth and Families, Children’s Bureau. (2023). Child Maltreatment 2021. Available from https://www.acf.hhs.gov/cb/data-research/child-maltreatment.

[2] https://www.childrensdefense.org/the-state-of-americas-children/soac-2023-child-welfare/

[3] Annie E. Casey Foundation, Child Maltreatment Trends: A Persistent Picture of Young Survivors and Neglect, August 9, 2023, https://www.aecf.org/blog/child-maltreatment-trends

[4] U.S. Department of Health & Human Services, Child Maltreatment 2021, (2023).

[5] Hunter, Amy and Flores, Glenn, “Social determinants of health and child maltreatment: a systematic review, Pediatric Research, 89-269-274, 2021.

[6] World Health Organization, Child maltreatment, September 12, 2022; https://www.who.int/news-room/fact-sheets/detail/child-maltreatment

[7] https://www.census.gov/content/dam/Census/library/working-papers/2022/demo/sehsd-wp2022-24.pdf

[8] Unlike the U.S. Census Bureau’s Official Poverty Measure, the SPM takes into account expenditures for food, clothing shelter, and child care (among other areas) as well as income from tax credits and other sources such housing subsidies, the Supplemental Nutrition Assistance Program, and the nutrition program under the Women, Infants, and Children (WIC) Program.

[9] https://www.census.gov/library/publications/2023/demo/p60-280.html

[10] U.S. Census Bureau, Supplemental Poverty Estimate using American Community Survey Public Use Data

[11] U.S. Census Bureau, 1-Year American Community Survey Data, 2022.

[12] Weiner, D.A, Anderson, C. and Thomas, K. (2021). System transformation to support child and family well-being: The central role of economic and concrete supports. Chicago, IL: Chapin Hall at the University of Chicago

[13] Bullinger, Lindsey Rose, and Boy, Angela. (2023). Association of Expanded Child Tax Credit Payments With Child Abuse and Neglect Emergency Department Visits. JAMA Network Open. 2023;6(2):e2255639

[14] Kovski NL, Hill HD, Mooney SJ, Rivara FP, Morgan ER, Rowhani-Rahbar A. Association of State-Level Earned Income Tax Credits With Rates of Reported Child Maltreatment, 2004-2017. Child Maltreat. 2022 Aug;27(3):325-333.

[15] Klevens J, Schmidt B, Luo F, Xu L, Ports KA, Lee RD. Effect of the Earned Income Tax Credit on Hospital Admissions for Pediatric Abusive Head Trauma, 1995-2013. Public Health Rep. 2017 Jul/Aug;132(4):505-511.

[16] Rostad, W. L., Ports, K. A., Tang, S., & Klevens, J. (2020). Reducing the Number of Children Entering Foster Care: Effects of State Earned Income Tax Credits. Child Maltreatment, 25(4), 393-397.

[17] Spencer RA, Livingston MD, Komro KA, Sroczynski N, Rentmeester ST, Woods-Jaeger B. Association between Temporary Assistance for Needy Families (TANF) and child maltreatment among a cohort of fragile families. Child Abuse Negl. 2021 Oct;120:105186.

[18] In 2023, Arizona had a one-time tax rebate program in place. Qualifying taxpayers could receive a rebate of $250 per dependent under age 17 and $100 per dependent over age 17 as claimed on their 2021 returns. The maximum available rebate for taxpayer was $750.

Census figures show more than one million Illinois children were below 250% FPL in 2021.

Census figures show more than one million Illinois children were below 250% FPL in 2021.

Census data shows the poorest Illinois residents are paying the most in rent. Housing is a necessity; it is not a luxury item. To be rent burdened means to be paying more than 30% of monthly income on rent. Currently, 44% of Illinois renters are rent burdened. Renters with the lowest income are also paying the most out of their pockets for rent. For Illinois households earning less than $20,000, 88.2% are rent burdened. For those households earning more $75,000 or more, just 5.3% are rent burdened. The numbers also differ by region, which is a factor of income as well as the stock of affordable housing. In Kendall County, 99.5% of those making under $20,000 are rent burdened.

Census data shows the poorest Illinois residents are paying the most in rent. Housing is a necessity; it is not a luxury item. To be rent burdened means to be paying more than 30% of monthly income on rent. Currently, 44% of Illinois renters are rent burdened. Renters with the lowest income are also paying the most out of their pockets for rent. For Illinois households earning less than $20,000, 88.2% are rent burdened. For those households earning more $75,000 or more, just 5.3% are rent burdened. The numbers also differ by region, which is a factor of income as well as the stock of affordable housing. In Kendall County, 99.5% of those making under $20,000 are rent burdened.